US Manufacturing Is Genuinely Expanding Again

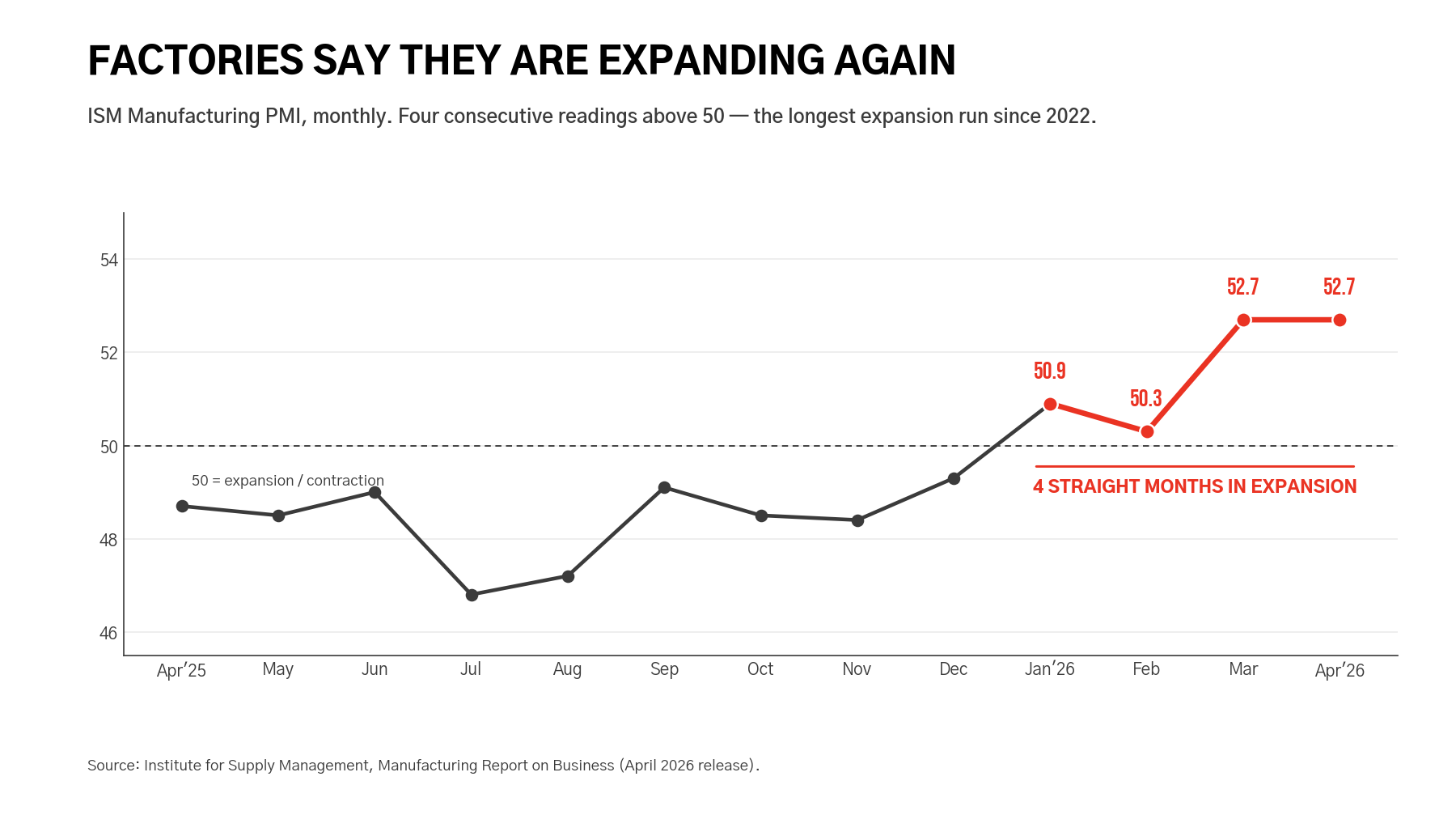

US manufacturing has spent most of 2025 in contraction. That just changed. The April 2026 ISM Manufacturing PMI printed at 52.7, matching March and marking the fourth consecutive month the index has read above 50 — the cleanest expansion run since the summer of 2022. New orders accelerated for the fourth straight month. The Production Index has now expanded for six months running. The signal is broad: 13 of 18 manufacturing industries reported growth in April.

That is the soft data — what factory managers say. The hard data agrees, with a wrinkle worth understanding.

US private factory construction spending ran at a $189B seasonally-adjusted annual rate in March 2026, per the Census Bureau. That is below the $239B peak hit in July 2024 (the high-water mark of the CHIPS Act and IRA buildout), but it is roughly 2.5x the pre-CHIPS baseline of $76B in January 2021 — and it has held above that 2.5x line for nearly two years. We are not building new factories at peak speed any more. We are building them at twice and a half the rate we used to build them, every month, for two years running. That is the difference between a project pipeline and a structural shift.

The composition is also changing. Construction of chemical-products factories rose 9.9% year-over-year to $46B SAAR in March, the second-largest factory subcategory and the one most directly tied to industrial reshoring of materials. Construction of semiconductor and electronics factories has eased from its 2024 peak — but a second wave is now visibly lining up, including SpaceX's Terafab facility in Grimes County, Texas (announced first-phase capital investment ~$55B) and Micron's flagship memory complex in Clay, New York.

So the picture is this: PMI says factories are growing again, after a contraction year. Census spending says we are still building new ones at a historically elevated pace. Both signals usually move together; right now, they agree. That is rare.

For founders, especially in industrial software, robotics, supply-chain tooling, and energy infrastructure, this is the macro tailwind we have been underwriting to since 2022 — and it is becoming legible in operating data, not just announcements. For LPs, the cleanest read is to look past the headline-vs-2024-peak comparison: the right baseline is 2021, and against it, the US manufacturing base is expanding by every measure we track.

At Interplay we underwrite to this base case.

Sources

- ISM, Manufacturing Report on Business — April 2026. ismworld.org. PMI 52.7, fourth straight month in expansion; New Orders 54.1; Production 53.4; 13 of 18 industries reporting growth.

- US Census Bureau, Construction Spending — March 2026. census.gov. Total construction $2,185.5B SAAR; private manufacturing construction $189B SAAR; chemical-products factories +9.9% YoY to $46B SAAR.

- FRED, Total Construction Spending: Manufacturing in the United States (TLMFGCONS). fred.stlouisfed.org. Series sourced from US Census Bureau; used for the 2021–2026 monthly trajectory.

- Wolf Street, Construction Spending on Data Centers, Factories, Chip Plants, Powerplants, Office Buildings. wolfstreet.com. Subcategory breakdowns and second-wave context (SpaceX Terafab $55B first-phase / Micron Clay NY).