The New Exit: Secondaries

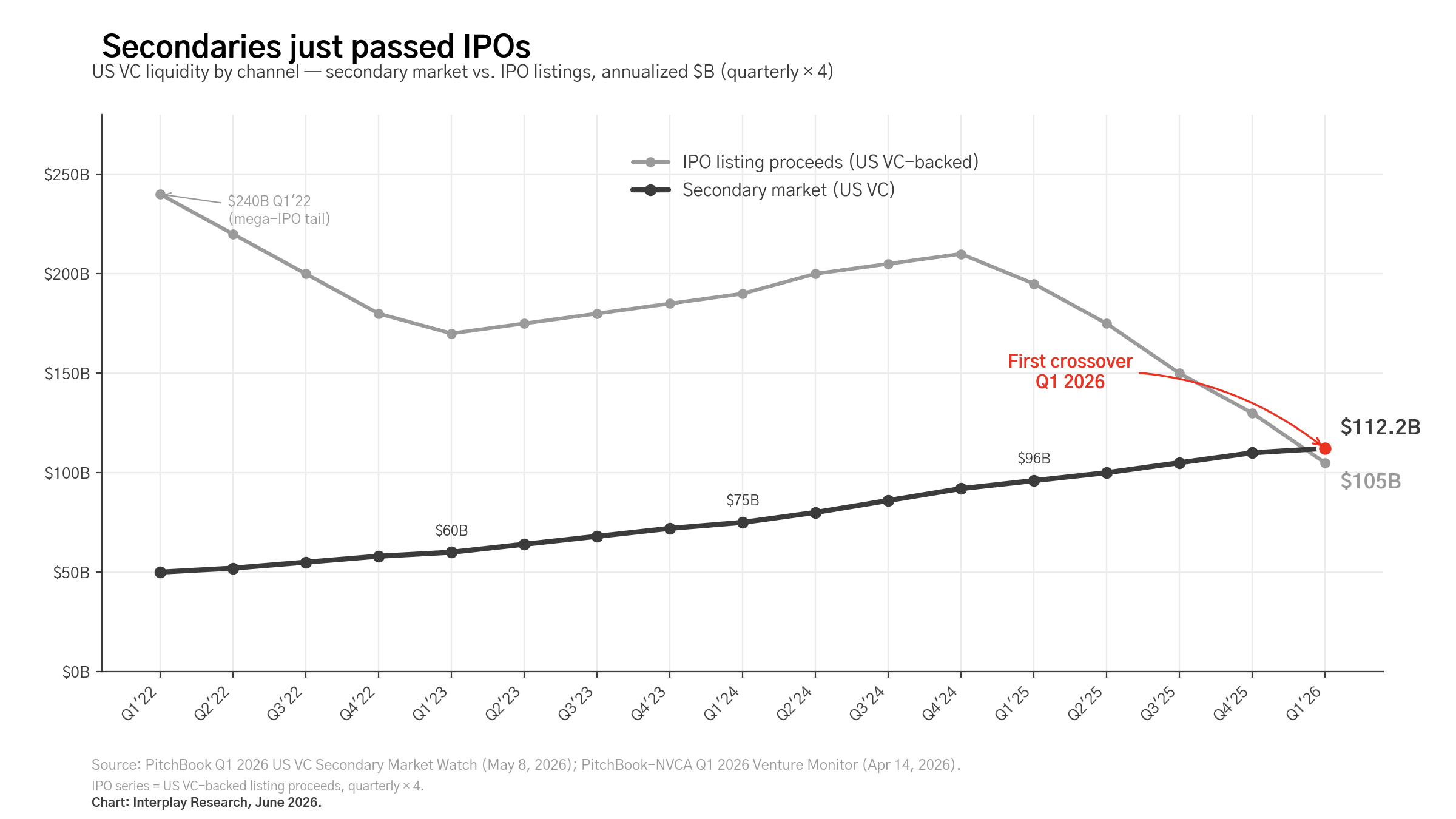

On May 8, 2026, the research firm PitchBook published its Q1 report on US venture-capital share sales and slipped one sentence into the summary that, on its own, may be the most important venture finance number of the last decade: in Q1, the value of private share sales between investors reached an annualized $112.2 billion and was larger than the total raised by US venture-backed companies going public.[1] In plain terms, more dollars came back to investors through private share trades — employees selling to a fund, one fund buying out another, founders selling a slice of their stock — than through traditional stock-market listings.[2] The way venture money has historically come home — a big IPO bell-ringing moment — is no longer the main path.

This isn’t just because the IPO market has been quiet. Private share sales have grown by roughly 30 percent a year since 2022, while IPO proceeds have stayed roughly flat. PitchBook’s own outlook calls 2026 a “defining year” — the moment private share sales graduate from a temporary fix into a permanent piece of how the venture market works.[3] The pool of money set aside specifically to buy these private shares hit $11.8 billion in June 2025, nearly three times what it was in 2022, and it’s still climbing.[4] This is a structural change, not a workaround.

For venture capital fund managers, the way they return cash to their own investors just changed. Historically, a fund showed real results only when one of its companies went public or got bought — sometimes a decade after the original investment. Private share sales let a fund send cash back to its investors years before any of that happens. The trade-off: every time a sale prints a real price, the fund’s books have to reflect that price, up or down. So managers get faster wins but also feel the pain of bad quarters sooner, while the fund is still active.

For the institutions that put money into those funds — pensions, endowments, family offices — the bigger shift is on the other side of that same coin. The “value” line on a quarterly report used to be an estimate. Now, increasingly, it’s a real price someone just paid. That’s good news: investors can finally trust their venture numbers the way they trust public-stock numbers. The catch is that those numbers can also move 30 percent in a single quarter without a company doing anything new — purely because the private market re-priced it.

For founders, the change is most visible inside their own companies. Tender offers — where a company sets up a one-time window for employees and early investors to sell some shares — used to be a rare treat at the most senior level. Now they’re regular events at well-funded private companies. That changes hiring (early engineers no longer have to wait a decade to see anything), it changes how concentrated founders are in their own company (founder sell-downs are now standard at the late stage), and it changes the calculus on going public at all. Why ring the bell on a giant public listing when more than $112 billion a year now changes hands quietly inside the private market?

The big IPO class PitchBook is forecasting — SpaceX, OpenAI, Anthropic — will reset this picture in 2026 and 2027.[5] But “reset” is the right word, not “reverse.” Private share sales aren’t going away after those companies list. The plumbing has already been built. The new exit — secondaries — has quietly become the exit that might just matter the most.

Sources

- [1] PitchBook, "Q1 2026 US VC Secondary Market Watch" (May 8, 2026). pitchbook.com

- [2] PitchBook-NVCA, "Q1 2026 Venture Monitor" (April 14, 2026). nvca.org

- [3] PitchBook, "2025 Annual US VC Secondary Market Watch" (Feb 23, 2026). pitchbook.com

- [4] PitchBook (via Yahoo Finance), "2026’s fast-approaching mega-IPO wave is expected to reset the VC secondaries market" (April 22, 2026). finance.yahoo.com

- [5] PitchBook, "Q1 2026 PitchBook Analyst Note: 2026 IPO Outlook for US VC" (January 26, 2026). pitchbook.com