Manufacturing Is Growing on Automation + AI, Not Headcount

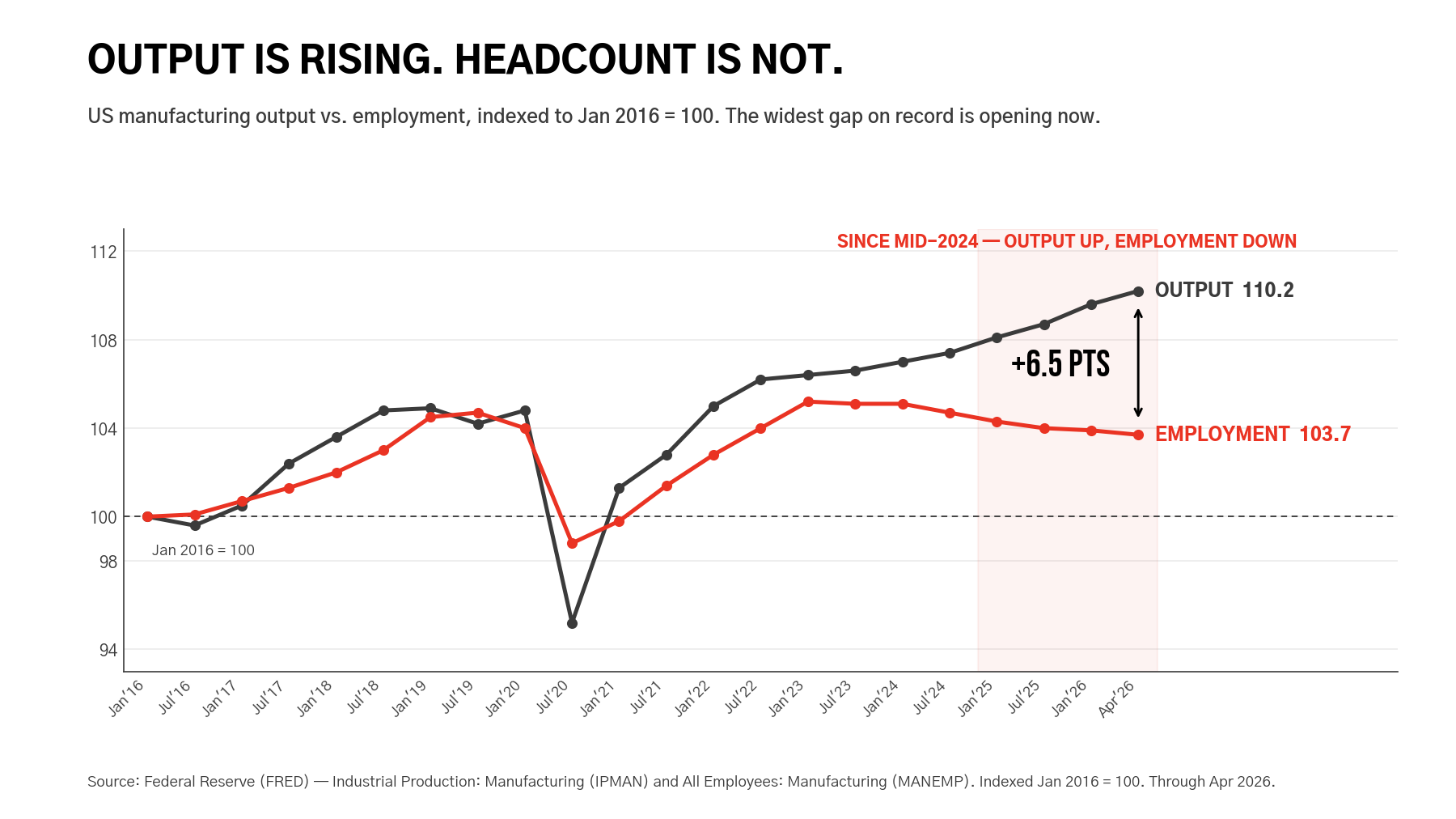

US manufacturing output (Industrial Production: Manufacturing, FRED IPMAN) has risen to 110.2 on a January-2016 base — a fresh high. US manufacturing employment (All Employees: Manufacturing, FRED MANEMP) sits at 103.7 on the same base, down from a 2023 peak near 105.2. The gap is now ~6.5 index points, the widest on record, and almost all of the widening has come in the last 18 months.

The April 2026 ISM Manufacturing PMI confirms the soft data. Headline PMI printed 52.7, a fourth straight month in expansion. But the Employment sub-index has been in contraction (<50) for 22 of the last 24 months, including April 2026 at 46.8. Factories say they are producing more. They also say they are not hiring to do it.

The Q1 2026 BLS productivity release closes the loop. Manufacturing labor productivity rose 3.6% annualized in Q1 — 5x the nonfarm business rate of 0.8%. Output rose 3.3%; hours worked fell. That is the textbook definition of automation taking on marginal load — the same dollar of output, with less labor behind it.

The capital is following. The US Census Annual Capital Expenditures Survey shows manufacturing capex of $314.3B in 2022 (most recent vintage), with US capex on robotic equipment specifically at $12.96B. The IFR's 2024 vintage release puts US manufacturing robot density at 307 robots per 10,000 employees, up ~4% YoY — ranking the US 8th globally and rising.

The takeaway for Interplay: this is the macro tailwind we have been underwriting to since 2022, now legible in operating data instead of forward-looking announcements. Manufacturing is genuinely expanding. It is expanding with materially more output per worker than the rest of the economy. And it is doing so on equipment + software, not headcount.

For founders building industrial AI, factory robotics, MES/QC software, vision systems, predictive-maintenance, and the workforce-augmentation layer around all of the above — the addressable spend is now showing up in the BLS and Census prints, not just the slide decks. For LPs, the cleanest read is that the productivity dividend the macro data has been missing has, in fact, arrived — it is just sector-specific. Manufacturing has it. Most of the rest of the economy still doesn't.

At Interplay we underwrite to this base case.

Sources

- Federal Reserve — Industrial Production: Manufacturing (FRED IPMAN). Monthly index, NAICS basis; April 2026 release. fred.stlouisfed.org/series/IPMAN

- Federal Reserve — All Employees: Manufacturing (FRED MANEMP). Monthly, BLS source; April 2026 release. fred.stlouisfed.org/series/MANEMP

- BLS — Productivity and Costs, First Quarter 2026, Preliminary. May 7, 2026 release. Manufacturing labor productivity +3.6% (annualized); output +3.3%; hours worked declined; nonfarm business productivity +0.8%. bls.gov/news.release/prod2.nr0.htm

- ISM — Manufacturing Report on Business, April 2026. PMI 52.7 (4th straight month in expansion); Employment sub-index 46.8 (24-month series shows contraction in 22 of last 24 months). ismworld.org/supply-management-news-and-reports/reports/ism-pmi-reports/pmi/april/

- US Census Bureau — Annual Capital Expenditures Survey (ACES), 2022. Manufacturing sector capex $314.3B; US robotic-equipment capex $12.96B (statistically unchanged vs. 2021). census.gov/programs-surveys/aces.html

- International Federation of Robotics — Robot Density 2024. US manufacturing robot density 307 robots per 10,000 employees (2024 vintage, released April 2026); North America up ~4% YoY. ifr.org/ifr-press-releases/news/robot-density-surges-in-europe-asia-and-americas